How To Do Things With Rates

Where do interest rates come from and what do they organize? Are they causes? Effects? Both? A secret fourth thing?

What concerns are operative when the economy is disorganized? The state of aggregate demand right now (early 2026) is deeply uncertain. Job growth is decelerating but households are spending and business investment is strong. The US housing market is suffering from what appears to be intertemporal disorganization. The “Big Fiscal” policies of 2020 reset household balance sheets, setting up housing to face demand, rather than financing constraints. This supported a wave of investment into new homes. Now that those investments are congealing into finished or near-finished houses, there is a large, segment-specific new housing glut, at least by some inventory measures. This glut is also taking place within an overall housing shortage, believed to originate from structural concerns rather than the business cycle. We seem to have conflicting stories here.

You may be familiar with the idea that temporal disorganization comes from distortions, but not the usual distortions of, say, taxes creating deadweight loss. Rather, some economically literate people have strong opinions on the fact that the tone of Fed communications has measurable effects on asset prices, which they feel should depend on economic fundamentals. They regard the apparent temporal disorganization in the market for complex capital goods such as homes and so-called human capital - which is seemingly caused by central banks shifting priority from stimulating demand to lowering prices - as a dangerous disconnection from underlying economic conditions. That disorganization happened, some of them believe, specifically because of shifts in the interest rate. Perhaps if the interest rate was kept at a correct, steady rate then the intertemporal supply and demand for housing and labor would also be balanced.

But how do all these effects work in the first place? Why isn’t the interest rate just set by the balance of intertemporal supply and demand, independent of central bank jawboning? When mortgage rates reset faster than housing supply can respond, are interest rates operating as part of coordination failure or failing their unique role as a signal of “intertemporal scarcity” (whatever that is)? In short, “In what sense are interest rates causes and in what sense are they effects?”. At their worst, these concerns can drift toward attempts to treat certain financial assets as monetary benchmarks, even when their volatility or illiquidity prevents them from functioning as discounting or hurdle rates.

Though more important to discuss the economy than economics, all these questions turn on the economics question of “what sets interest rates?”. We are back to our original question: what concerns (balance-sheets, optionality, margins, rollover, funding risk, etc.) are operative when things are “disorganized?”

Since we are moving into the abstract, let’s set up the table with a core principle. This is our solid methodological plate on which we can place softer and gooier ideas without making a mess: AN INTEREST RATE IS A RELATIVE PRICE. Whenever you’re confused about capital or interest rates, try this: leave the computer, take a deep breath, relax your eyes, unclench your jaw and remind yourself “An interest rate is a relative price.”

Because interest rates are real market activities, we aren’t able to assume a priori that they perform a particular activity. Maybe they play a role in coordinating market activity in the face of complexity or fundamental uncertainty, maybe not. Maybe they are downstream of deep economic fundamentals like technical progress, capital accumulation and fundamental psychological necessity - or maybe upstream or both or neither. Maybe there is a special interest rate that sets the tone for all the others, or maybe not. Hey, maybe all prices do is conceal exploitation under the flag of profit-seeking and so mystify the relations of production. The principle of “quantifying the quantifiable” only helps us choose what to investigate, not answer what that thing is.

What we can assume is that whatever role interest rates play can be discovered in markets themselves. What matters for market participants is what the rate embedded in a 30-year mortgage, a Secured Overnight Financing Rate (SOFR) swap or a Treasury future is functioning as, not what it could function as.

You see, as relative prices, interest rates are part of the objective economic world, not deep, hidden parameters or deep, hidden residuals. Of course expectations, conventions and uncertainty matter to their determination but the interest rate written into a contract, the outcome, is a quantifiable fact. When going from interest rates to the interest rate, follow the principle of quantifying the quantifiable. Interest rates are quantifiable and observable, don’t give them up for the invisible and unobservable. Use them as guides for the invisible and unobservable.

The principle of “quantifying the quantifiable” is thus not a dismissal of the complex and unobservable. Rather, the goal is to hold onto those few firm bits we do have in a complex, dynamic and uncertain reality. This principle is worth insisting on, as it is deeply important to market analysis that interest rates are market variables, not themselves psychological parameters nor invisible residuals.

The interest rates built into those housing market contracts aren’t parameters or residuals - they are actual relative prices. The actual interest rates embedded in financial contracts and which drive investment decisions can be a ground for analysis in the face of complexity and fundamental uncertainty. Again, a 30-year fixed mortgage, a SOFR-indexed construction loan, and a Treasury future all embed interest rates as tradable relative prices, not inferred parameters. That ground is what is risked in giving them up.

Of course, there are unboundedly many relative prices - like the ratio of the prices of grapes and grape-nuts. They are not all interest rates. Interest rates are distinguished from random price ratios by the fact they can be meaningfully used to discount income flows. This is how interest rates are defined by their roles in economic practice.

Examining a financial contract, we discover that an interest rate is, in the simplest case, the ratio of the difference between the future price of a service flow and the spot price of that service to the spot price of the service. If you switch future and spot then you get a discount factor. Because the discount rate has a simple algebraic relationship with the interest rate, I’ll sometimes use the terms interchangeably.

I am insisting on this objectivity point at length because it can be very difficult for people to differentiate between the fact of an interest rate with their theory of the interest rate. It is all too easy to slide between “interest as a price” and “interest as a conceptual object” without noticing the shift. As Continuous Variation (CVAR) Editor Alex Williams noted, the interest rate is a central and load bearing structure in economics. Given the interest rate, economics has predictive power across wide domains - in micro domains (when will kids mow a lawn today for a pie tomorrow), in growth theory (what technologies will be invested in) and in macro domains (how many millions should be unemployed). Milton Friedman won a Nobel Prize in work that included finding a (fairly weak) effect of the interest rate in the consumption function. But conditional predictions given the rate of interest are much stronger than predictions of the rate of interest itself (because comparative statics require fixed rates). This is a delicate situation in a fundamental part of market analysis.

We therefore can see why there is an impulse to keep such a load-bearing structure safe from empirical revision. But that temptation must be resisted. In fact, we must ask ourselves, is there even really a “the interest rate” in addition to interest rates at all?

The Classical Theory: Knight’s “Capital, Time and the Interest Rate”

We can start with the question of why there is “the interest rate” by answering what the so-called classical (or neo-classical) theories of the interest rate even were. This will land us with Keynes eventually via a roundabout process while demonstrating both that his critique is non-empty and the benefits of his positive theory. The cost is that occasionally there will be long strings of strange names that seem to have nothing to do with market analysis. I believe this cost to be worth getting a feeling of the vast literature that existed even in Keynes’ time and therefore the trade-offs he had to consider in making analytical choices. However, I will try to keep things in real market behavior as much as possible.

Leaving markets just for a moment, Keynes (in “Alternative Theories of the Rate of Interest”) talks a bit about his own intellectual genealogy. He explicitly names Fisher as the origin of his thinking: Fisher -> Hawtrey -> Robertson -> Keynes. We won’t take this route because these thinkers tended to be analytically dense rather than lend themselves to a straightforward exposition. Richard Kahn’s book The Making Of Keynes’ General Theory goes through that genealogical process in detail.

Coming back to pre Keynesian theories of interest, we will find that, like all classical theories, the classical theory of the interest rate is concerned with the causes of price - why does the interest rate exist at all? What classical economists meant by this question is subtle. In market terms, the relative prices of spot and future contracts have a marketwide tendency to correlate. While there are many idiosyncratic forces which shift interest rates in individual financial contracts, the correlation is strong enough that one can talk of a period of interest rates declining or rising altogether. However, that correlation alone does not tell us what anchors the rate. Again, back in the introduction, we saw a money market interest rate drive the housing interest rate rather than shifts in the physical costs of housing production.

Irving Fisher’s genius was to explain this via “intertemporal arbitrage”. If a particular good happened to have a persistently unusually good interest rate, then the actors on the market would be best off if they only bought futures in that good and then bought other goods on the spot market when they needed them. Of course, this simple thought experiment ignores important issues like finance, liquidity and fundamental uncertainty. Fisher was very clear that he considered this an approximation. Frank Knight in Risk, Uncertainty and Profit calls attention to what he calls the “Hegelian contradiction” in all this: intertemporal arbitrage equalizes rates but if rates are equal there are no arbitrage profits to be made. Modern finance theory has deeply analyzed these questions in logical and quantitative terms.

Turning back the clock is justified by clarity rather than depth. And so, I will go with Frank Knight’s exposition in “Capital, Time and Interest” because Knight’s aim of foundational clarity rather than analytic breadth suits our purposes.

Knight’s targets in this paper are the theories of interest descended from that developed by Englishman William Stanley Jevons. These would be picked up by Austrian economist and finance minister Eugen von Bohm-Bawek in an exposition so foundational that they became known as “Austrian” theories (though they were actually developed internationally).

Leaving behind the name issue, the distinction between these lineages is well captured by their answer to the question “What is capital?”. Fisher defined capital as income-producing assets while Jevons defined capital (technically, the “amount of investment of capital”) as the sum of physical inputs to the wage fund multiplied by the length of time of the average period of production. You can probably tell which of these is more fundamental for market analysis.

Moving into said market analysis, the theory of the Jevons side of the family tree, as expounded by Böhm-Bawerk, identified three causes of interest. I will give each of these causes and how they can be tied to the housing market. These mechanisms are not offered as literal descriptions of how market interest rates are set, but as the conceptual foundations Böhm-Bawerk believed must underlie any coherent theory of interest.

Pure time preference: present income is valued more highly than future income (holding quantities constant) for fundamental psychological reasons.

Putting money into an account to create a wage fund for workers on a house over time means less consumption today. Thus profits must be high enough tomorrow to justify that loss.

Pure technical progress (“roundaboutness”): longer and more capital-intensive production processes yield a greater physical output, which makes waiting economically advantageous. That waiting must be compensated if such processes are to be undertaken.

The inputs to housing (like electrical equipment and plumbing) improve over time. What used to be done with a hacksaw can be done with a Sawzall. Those improved equipment are, at least qualitatively, the result of longer-cycle capital which - allegedly - must be maintained with an interest rate.

Technical-progress-adjusted time preference (“wealth effects on valuation”, “agio”): the marginal utility of income falls over time as people expect to have greater wealth in the future due to the accumulation of capital.

As the stock of capital rises, the price of equipment like nails and wire falls. Thus we need a premium on present goods, which manifests as interest.

Theorists in this “Austrian” school vary on the process of how these forces (all of which are very real) work themselves out, as well as the question of which is the most fundamental, etc.. But all “Austrian” theories agree on the existence of an “interest rate” determined by productivities, fundamental psychology, capital structure and the stock of wealth - the natural rate of interest. This idea of a given ‘natural rate’ which actual interest rates can equal or not is the source of the diagnosis of housing supply issues as temporal disorganization from the introduction.

We now turn from exposition to criticism. Knight is correct to point out that the empirical and logical arguments for these sources for interest rates are weak as determinants of an observable market rate rather than as background conditions. Let’s go through them one by one.

First pure time preference: this theory is - to the extent it is not wrong - circular. One cannot meaningfully explain interest by interest by presupposing discounting. These two concepts are simple algebraic transformations of one another. Further, people trade consumption across time depending on many local factors such as wealth, risks peculiar to different income-producing instruments and the opportunities available. Every person and every good should have a constantly shifting discount rate, not one market rate. If there is a market mechanism to harmonize psychological discounting then the mechanism is doing all the work, not time preference.

Next, roundaboutness: as old-growth forests are increasingly harvested, the quality of wood has declined but there is still a positive interest rate in lumber markets. Lumber is an important input to housing markets, showing that this declining roundaboutness is not driving rates. Roundaboutness or technical progress cannot by itself explain why there is a dominant and positive market interest rate. Even if roundaboutness is interpreted structurally rather than qualitatively, it does not explain why one ‘natural’ rate coordinates heterogeneous production processes. And to the extent that coordination happens, then the market coordination process is doing the work, not the roundaboutness itself.

Finally, the agio. On the one hand, wealth effects on valuation are simply the overlap with the previous two. But even if we allow this a non-circular place, why do wealth effects explain the correlation of market rates rather than act as a decorrelating force? Remember it was this correlation which the whole theory was designed to explain. But why can’t a wealthier society tomorrow push the interest rates on copper and gold wire apart rather than together? It seems that the wealth effects are just one market force among many, rather than fundamental. More broadly, the whole notion of technical progress as capital accumulation is highly questionable.

In each case, these mechanisms contribute to individual valuation, but none explains why a single ‘natural’ rate of interest coordinates heterogeneous assets across time. All of them are subject to idiosyncratic reversals at any time: A person who - perhaps by windfall gain - is in a position to consume more today than his psychology prefers will trade away some of their consumption today for income tomorrow. And yet market valuation means discounting that income like anyone else. Any attempt to ground interest rates in an absolute preference for consumption today breaks on this point.

Knight sees all this as sheer error; the word “fallacy” is never far from his lips. But the Böhm-Bawerk approach could be defended as a provisional and approximate place. Still, the methodological sign of what Knight sees as “error” is that in the Böhm-Bawerk system, the interest rate is treated as not an objective relative price found in financial contracts but rather a parameter. This is one of the twin pitfalls mentioned in the opening.

Continuing with Knight, he develops from his critique what he calls his five “main propositions” for the classical (Fisherian) theory of the interest rate. They are, in his order:

The quantity of capital is equal to the present value of income generated by that capital discounted by a uniform rate.

The quantity of capital is equal to its construction cost = physical (opportunity) cost + carrying charge to entrepreneur for taking on the risk/uncertainty of holding that capital.

The value of the carrying (opportunity) cost is discounted at the same rate as physical cost.

The rate of discounting construction cost is the same as discounting income.

Any creation of an income yielding item is made “under the assumption that the [discounting] rate is the maximum possible under the technical circumstances … of the economic situation in which it is made.”.

Knight would not deny his “main propositions” include important simplifications. But still, his “main propositions” power a transparent theory of interest rate based on the market valuation of income-producing instruments. So far, the interest rate is a relative price. Valuations are primary, psychology and technology matter to the extent they affect valuation.

From a Keynesian perspective, the first four assumptions are acceptable, with similar caveats as Knight or Fisher themselves would make. To see this in terms of Keynes’ first postulate of classical economics (which Keynes provisionally accepts), remember that Knight treats labor as just one form of capital.

But the last assumption is key to making this a (Keynes’ sense) classical theory of interest: it is equivalent to effective-demand full employment. Knight does not allow for the depression condition of shoeless children whose parents have been fired from the shoe factory. Thus Keynes cannot agree with Knight’s “main propositions” in the manner Knight uses them.

Knight’s assumption implies a scarcity in intertemporal exchange under competitive markets - the only way to create more income tomorrow is to “invest” rather than consume today. Income tomorrow is treated as technologically determined rather than allowing for demand constraints.

But this moves us away from market valuation. To paraphrase Keynes, Knight’s fifth assumption means that under free competition “the utility of the price of capital goods when a given volume of capital goods are employed is equal to the marginal disutility of that amount of employment.”. With Knight’s notion of labor as capital, this really does become Keynes’ “second postulate of classical economics”.

This all has gotten very abstract. How does it all shake out for market analysis? Again, by the means of his assumptions, Knight is able to ground interest rates in the equilibrium of competitive intertemporal markets, not the improving technology or the psychology of time preference. Interest rates are prices, not parameters. This is a great insight and Knight is right to insist on it and its consequences.

But how does he explain the empirical fact that interest rates are a spectrum which depend on the peculiarities of particular investments? If spot and future prices are both heterogeneous in an economically meaningful way, then interest rates must differ. Knight could reply: “if different assets truly carry different effective discount rates, then what you are calling ‘interest’ is no longer interest proper but a mixture of pure interest, risk and uncertainty.”.

But the Keynesian has a devastating countercritique: what Knight is calling the interest rate is no longer within the objective market reality of relative prices! Knight defines the interest rate as what remains after abstracting from risk and uncertainty, but that is not what is written in financial contracts. He has fallen into the trap of regarding the interest rate as a residual, not an actual price ratio. This is equally dangerous as treating interest rate as a parameter.

The residual vs. parameter issue is part of the reason that the debate between Knight and Hayek seemed interminable. Maybe Knight’s theory of interest has advantages as an explanation of interest as a market variable. But his residual is defined by a limit concept, and that limit never occurs in real markets. Knight then implicitly issues a vague promise that the rest of the way to observed prices will be covered by some continuity principle.

Hayek, Knight’s direct opponent in this paper, simply prefers to start with time preference as a first approximation. He also implicitly relies on a vague promise that the rest of the way to observed prices will be covered by a similar continuity principle. Hayek’s approach certainly has its own advantages. After all, Hayek wants to work away from the market equilibria Knight focuses on. Who is to say which advantage is decisive?

Coming back to methodology, the principle we call quantifying the quantifiable is key to getting past this impasse. Keynes was only able to hold to his principles and avoid these dual pitfalls by making fundamental changes to the standard tools of market analysis.

Keynes’ Critique of Untheory

In the introduction, we asked the basic question of which operative factors determine interest rates whether or not the market is temporally organized. In the last section, we went over some interest rate concepts which seemed inadequate for market analysis - namely they turned interest rates into parameters or residuals rather than real market variables. We know from history that Keynes needed to change certain fundamental tools of market analysis in order to solve this conceptual issue.

Before we go into details of those changes, I’d like to give an overview of Keynes’ concept of what we now call “the macroeconomy”. Keynes’ chief concerns are with the stock of money (in a given year), the stock of employed labor, the rate of money-wages and the flow of money income. These are the kind of economic realities that you recognize at a macro desk. What we see is that Keynes will not offer a control theory of the economy here (changes in the stock of money do not mechanically change the money wage or money income), but a diagnostic logic for understanding the level to which prices and his fundamental variables tend to stabilize under uncertainty and seeming “discoordination”.

Let’s pause and center ourselves in Keynes’ tests. Keynes discusses interest rates in Chapter 13 (see also) and their connection to capital in Chapter 17 (see also). The central devices which Keynes uses to analyze capital are “liquidity preference” and the “own-rates of interest”. Together with what Keynes calls the “schedule of the marginal efficiency of capital”, a money-denominated schedule governing investment decisions from chapter 11, these elements complete Keynes’ theoretical system.

These arguments have deep logical interdependence. Keynes’ notion of a schedule of marginal efficiency of capital is very different from a typical productivity curve: the marginal efficiency curve is financial first and foremost. We need to establish the deep foundations first so that modeling decisions are properly motivated rather than smuggled in.

I didn’t make the decision to insist on these details lightly. Misunderstanding the modeling decisions has caused people to misunderstand Keynes’ system. We see this historically: in the wake of Keynes’ General Theory, there was a flood of claims that Such And Such Writer/Tradition Knew It All Along. They even did this to Keynes’ face, see his “Alternative Theories of the Interest Rate” for a class of such claims.

To understand Keynes’ modeling decisions, we will run through Keynes’ Chapter 2 (see also). These are about the stock of employment, not interest rates but we can link these to interest rates and capital. It will remind us that “Yes, Virginia, There Was A Keynesian Revolution”, what the revolution was and why it was needed. Then the modeling decisions will be more comprehensible.

In Chapter 2, Keynes separated two claims which play deep, structural roles in what he called ‘classical theory’. Those claims are:

Wages (and prices generally) equal marginal product

The volume of labor (and inputs generally) is a function of the marginal product.

Today, we would not call these “postulates” as Keynes did. The postulates of our concept of ‘classical theory’ would be more like consistent preference rankings, convex production functions, etc.. Even at the time, Leontief interpreted Keynes’ core claim in a modern way: as the labour supply function not being homogeneous of degree zero in wages & prices (a characterization Keynes accepts in “The General Theory of Employment”).

Despite that, Keynes’ postulates still play an important role in the structure and interpretation of many modern marginalist economic frameworks. Keynes’s postulates no longer enter as behavioral axioms, but as “closure conditions” for market analysis. Thus Keynes’ approach to closure conditions is still very relevant to modern economics.

The first postulate Keynes’ provisionally accepts as a shorthand for sound market analysis. Notice that the first postulate (wages = marginal product) is an attempt to find an observable market anchor for labor, quantifying the quantifiable. Going deeper than this postulate is possible. Joan Robinson showed how Keynes’ system can be employed for a deep analysis of wage determination by investigating the feedback of wages onto profits, general equilibrium and imperfect competition. But in terms of investigating Keynes’ relation to classical theory, it’s best to just follow Keynes and provisionally accept the first postulate ‘with the usual caveats’.

Moving on to the second postulate, which Keynes rejects. There has been evasion on this issue, but the claimed causality from marginal product onto level of employment is indeed a part of classical economics. Even those who saw issues (including Fisher and Hayek above) did not build an explicit, operational replacement for the second postulate’s closure conditions.

That the second postulate was part of classical economics at all can be shown reading the relevant texts and by logical analysis. Starting with a clear textual example, that “purist of marginal theory”, Philip Wicksteed, puts the second postulate and its consequences bluntly in The Common Sense Of Political Economy, Book 3:

We will now turn to the connected problems of unemployment, depression, and commercial crises, which are admittedly amongst the most baffling on the whole field of applied economic science. … Every one knows that persons, not without some dexterity both of mind and hand, may be absolutely unemployable in a given post. Every busy man has had embarrassing offers of “help” from zealous friends who are willing to do anything,—but who can do nothing that does not require more superintendence and correction than the result is worth. …If this fact could be universally recognised, one cause at least of unemployment would be removed or qualified; for it is obvious that the attempt to maintain a standard wage, or to fix a minimum wage, independently of fluctuations in the market of the product, must, so far as it succeeds, throw men out of work when the demand falls, until the marginal value of the reduced product and the marginal significance of the reduced number of workers bring about equilibrium.

I almost prefer Wicksteed’s plain admission of Keynes’ second postulate to the misty evasions that one sometimes encounters. But even without our good old honest Unitarian Minister Wicksteed, one can see through the mist - that is, the postulate can be seen to be a deep part of traditional theory directly.

We will start that direct path with the most solid step in the classical method: prices are set on the market. The solidity makes sense, prices are part of the objective world after all.

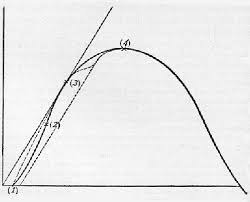

The next step is not as solid, but seems to be reasonable: given the prices, managers choose a level of input (say, labor) so that the marginal product of that input is equal to the price (with the usual caveats, of course). This relies on the notion of a “production function” independent of the market activity (Joan Robinson has an excellent critique of the implicit causal order). A typical qualitative example from Frank Knight’s Risk, Uncertainty and Profit is given below.

The x-axis is the number of labor hours per day and the y-axis is the apple output per day at a given plant. Region (1) to (2) is the region of increasing marginal product, after point (2) marginal product is monotonically decreasing. We can ignore region (1) to (2) as unstable in the sense that a firm can have more output (and thus profit) with the same marginal product for input levels between (2) and (4). Wicksteed, to give his point sharp definiteness, discusses the region after (4), negative marginal product but of course no rational manager chooses such a level of input usage. Wicksteed’s, and classical theory’s, real point is that there is exactly one volume of input where the marginal product is stably equal to the wage. In this manner, marginal product determines the volume of input and in particular labor usage - Keynes’s second postulate.

This analysis is, of course, partial equilibrium. The situation can change with general equilibrium. See, for example, IS-LM or more modern “general equilibrium with finance” models. But changing the model’s scope from single market to multimarket (from partial to general equilibrium) does not by itself change the underlying closure logic. Thus it is worth seeing Keynes’ general equilibrium thinking, so that we don’t lose track of sound economic reasoning when models become complex.

Now we’ve gone through Keynes’ Chapter 2. The question is now: How does Keynes’ second postulate tie to interest rate theory?

What is inexplicable in Wicksteed’s theory are the real facts of “depression, and commercial crisis”. On Monday, the shoe factory-employed parents and their children had shoes. Managers happily cited to Wicksteed and pointed to their production functions to explain their plentiful job creation. On Wednesday, the market collapses. On Friday, unemployed parents try to comfort their shoeless children while managers glumly cite Wicksteed and point to their production functions to show they are employing as many as they can. The technical facts of overcrowding (“too many cooks”) hold every day, independent of the level of employment.

This demonstrates the weakness of classical theories with respect to the business cycle. Similar paradoxes exist for problems of growth and monetary theory. All these issues have one thing in common: time. And time is also intimately tied to interest rates. Thus one can hope for a “General Theory” that will solve the problems of interest rates and business cycles. That’s what Keynes was able to do in the General Theory. Not because it is depression economics, but depression was a rare time where different theories of the interest rate act qualitatively differently. As said in the introduction, it was the lesion study which revealed the normal function in that area of the economic brain.

Of course, Keynes did not discover these issues for himself. There was already a vast literature on them, as the previous section’s parade of names demonstrated. To return to the above example, economics seems to work fine on Monday and Friday; it’s the comparison between them that breaks Wicksteed’s closure logic. Wicksteed’s logic holds pointwise in time (with the usual caveats), but fails across time. The standard pre-Keynesian reaction then was, as economist Paul Krugman discusses in his introduction to the General Theory, to move from foundational issues to complex dynamical models.

Some of these models were very insightful, such as Fisher’s concept of debt-deflation cycle (deflation->firms can no longer finance credit stably-> bankruptcy -> credit tightens -> deflation). But Fisher’s powerful intertemporal arbitrage tool becomes undone during debt deflation as interest rates deanchor. Krugman’s point is seen clearly through the questions “How can interest rates ‘deanchor’ in the first place? Aren’t interest rates set by intertemporal scarcity and physical productivities? The factory didn’t change from Monday to Friday, after all. So what sets the price of an asset, say a bond, during a period of debt deflation on Wednesday?”. Fancier models only hid the underlying flawed closure logic.

Krugman’s remarks are related to what economist and historian Gonçalo Fonseca calls Keynes Critique of Untheory. These ideas were rich, they were insightful but they were never part of the foundational structure of market analysis.

This is all becoming abstract again. Let’s look back at the week where we went from many shoes to few shoes. On Monday, there was an incentive to buy and hold shoes to sell for profit on Friday. Then there would never be a period of depression in the first place, just a seasonal production structure where production happens each Monday. So why wasn’t that investment actually made? Why did labor remain purely passive instead of saving? Obviously, the level of saving would be regulated by the interest rate: the future profit of holding shoes is discounted. Something had to raise the effective hurdle rate for carry.

In actual markets an interest rate, a risk premium or a liquidity premium/financing constraint can block intertemporal arbitrage. Classical economics can only bring in liquidity as a “rich insight” disconnected from fundamental theory. Liquidity would block the second postulate by making the level of employment a function of something other than the marginal disutility (i.e. by the financing). What they did was to treat liquidity as a sort of viscosity, effecting timing but somehow optional to fundamental closure logic.

Thus, ignoring liquidity as incidental to fundamental theory, we also see clearly a risk premium will not block our little example, the lack of shoes in the future is an opportunity not a risk. Perhaps if everyone buys shoes to save on Monday profits will be low (a “crowded trade”) but that’s still better than a depression. Thus the only systematic avenue consistent with classical closure to maintain a persistent arbitrage failure is a sudden spike in the interest rate. And now the determinism of classical theory becomes millstone: if the interest rate is set by time preference or productivities in market equilibrium, then there is nothing left to stop intertemporal arbitrage.

Knight has an answer to this: interest rates don’t need to spike to make depressions impossible because the future is uncertain! We didn’t know on Monday it would all collapse. The marginal parent is indifferent between saving another pair of shoes for an uncertain future and holding liquid purchasing power. And yet liquidity was presumed from the start not to be a concern. Knight was not clear on what he thought the alternative to investment is in the face of uncertainty if not liquidity. But, whatever the alternative to investment is a choice between, the marginal parent’s decision is influenced by current interest rates. Yet the interest rates that influence decision making are - necessarily - the objective price ratios, not unmeasurable parameters or residuals.

In this manner, we see how deadly the trap of making the interest rate into a parameter or a residual is. It’s important to see how this is specific to the interest rate. Economic analysis needs parameters and structural variables. But the interest rate cannot just be a parameter like the slope of the schedule of demand. True, demand schedules cannot be observed directly because they involve counterfactual situations (quantity demanded at prices that have not occured). But demand schedules have operational meaning in governing how observable prices respond to changes. They exist as shorthand for consumer based constraints on variation and can thus be inferred from market behavior even if not directly observed. Some (not all) market questions can be translated into subquestions of supply and demand theory. For instance, consider the question of seasonal cycles in the market for fish. The question of the quantity available at a given time as the seasons change the cost of fresh fish can be helpfully translated into statistical questions like “Is the demand schedule for canned saury stable? What about fresh?”. By contrast, Knightian interest has no obvious comparative statics nor does it constrain observable price movements in other ways. Though derived from market equilibrium, there is no market in which the rate itself clears.

To summarize, we have shown that if the interest rate is knowable and determined by productivity conditions, then intertemporal arbitrage destroys the possibility of a commercial crisis. There are twin pitfalls, determining before the market (as a parameter) or after (as a residual). In parameter theories, we have an invisible parameter as the true cause of all business crises - hardly an improvement on just calling the crisis exogenous. Meanwhile, Knight and related theorists’ reduction of interest rate theory to arguing about a residual has parallel issues. Knight consciously allows for leaving behind commercial crises, etc. for the mere analysis of supposed residuals. This amounts to willingly leaving market analysis behind for what Keynes calls “too easy, too useless a task” of telling us “that when the storm is long past the ocean is flat again”.

This is the impasse Keynes guides us through. We must ground capital theory in market analysis while breaking the second postulate, to allow for depressions, growth and monetary theory. That is not easy. Keynes’ was the beneficiary of both of his branches of ancestors - the Fisher side and the Jevons side - even if he wasn’t completely fair to one branch. But this interest rate economics was one of the fundamental tasks that Keynes’ needed to solve. We now turn to his solution.

Keynes’ Positive Theory Of Interest

In the introduction, we looked at some market puzzles to motivate our questions: why can we have inventory gluts amid scarcity? why do some financial instruments act as money and not others? We saw that these can be turned into the question “What is the interest rate?” We saw how classical approaches evade the market questions by making the interest rate into a parameter or a residual. And finally, in the previous section, we saw that the only way to fix this is by making fundamental changes to the process of market analysis. We have finally come to the time for positive theory: what are those changes Keynes had to make?

Keep reading with a 7-day free trial

Subscribe to Continuous Variation to keep reading this post and get 7 days of free access to the full post archives.